Provisional tax catches many new business owners off guard in Hong Kong. You file your profits tax return, receive your assessment, and then discover you also owe a second payment for the year that has not even ended yet. Understanding how provisional tax works, when it falls due, and how to legitimately reduce it can make a significant difference to your cash flow planning.

Highlights of this article

- Provisional tax is an advance payment of your next year's tax, estimated using the current year's assessment as the base

- The Inland Revenue Department (IRD) typically issues demand notes between November and January, with two instalments due roughly in January and April

- You can apply to hold over (reduce or defer) your provisional tax if your income is expected to fall by more than 10%

- Holdover applications must reach the IRD at least 28 days before the first instalment due date

- Late payment attracts a 5% surcharge, rising to a further 10% if the debt remains unpaid after six months

What Is Provisional Tax in Hong Kong?

Provisional tax is a forward-looking payment mechanism built into Hong Kong's tax system. When the Inland Revenue Department raises your final profits tax or salaries tax assessment for a given year of assessment, it simultaneously asks you to prepay an estimated amount for the following year. The estimate uses the current year's chargeable income as a proxy because the next year's actual income is not yet known.

It is important to understand what provisional tax is not. It is not a penalty, not a separate tax, and not an additional burden beyond your normal liability. When the IRD subsequently raises the actual assessment for the year in respect of which provisional tax was paid, the provisional tax already collected is credited (offset) against that assessment. If you overpaid, you receive a refund. If you underpaid, you pay the balance.

For more background on how profits tax is computed before provisional tax comes into the picture, see our complete guide to Hong Kong profits tax.

How Is Provisional Tax Calculated?

The starting point is the assessed chargeable income (or chargeable profits for corporations) from the most recently completed year of assessment.

For profits tax, the formula is straightforward:

| Step | Description |

|---|---|

| 1 | Take the assessable profits from the completed year |

| 2 | Apply the current profits tax rate (16.5% for corporations, 15% for unincorporated businesses) |

| 3 | The resulting figure is your provisional profits tax |

For salaries tax, the IRD estimates your employment income for the coming year based on the prior year, then applies the relevant rates or the standard rate of 15%, whichever is lower, after deducting applicable allowances.

The provisional tax demand note will show the computation clearly, including the base year, the estimated income, and the tax rate applied.

One nuance worth noting: taxpayers who submit their profits tax returns early (before the standard filing deadline) are often placed on a deferred payment schedule, meaning their demand notes arrive later and the instalment dates fall further into the year. This can provide a useful cash flow benefit for businesses that file promptly.

For more on the interaction between your tax return and your provisional assessment, see our guide on how to file a profits tax return in Hong Kong.

When Is Provisional Tax Due?

The IRD issues provisional tax demand notes alongside final assessments, typically between November and January each year. The demand note will state two specific instalment dates:

| Instalment | Proportion | Typical timing |

|---|---|---|

| First instalment | 75% of provisional tax | Around January to March |

| Second instalment | 25% of provisional tax | Around April to June |

The exact dates are printed on the demand note itself and vary depending on when the IRD processed your return. You should always verify the dates on your actual notice rather than relying on general estimates.

Payment can be made online via e-Tax, at PPS, at banks, or at the IRD's payment counters. Autopay arrangements can also be set up for businesses that prefer automated settlement.

How to Apply for a Holdover of Provisional Tax

A holdover (sometimes called a reduction) allows you to defer or reduce your provisional tax payment when you have valid grounds to believe your actual liability for the coming year will be materially lower than the estimate. This is one of the most practically valuable tools available to businesses with fluctuating income.

For a detailed step-by-step walkthrough of this process, see our dedicated article on holding over provisional tax in Hong Kong.

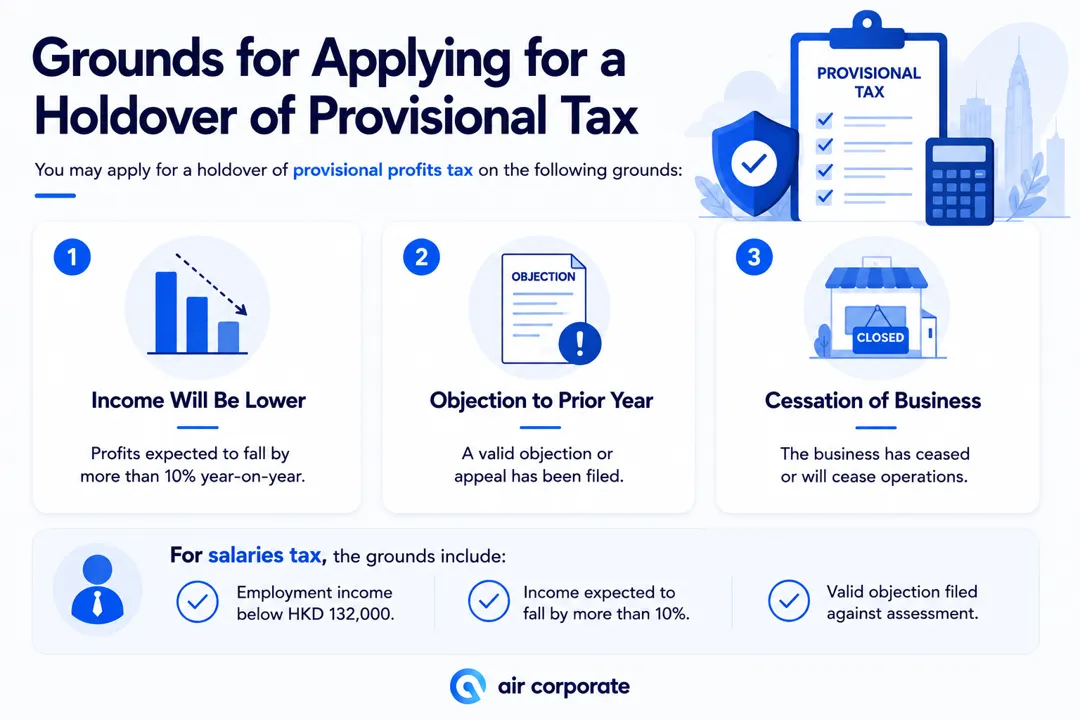

Grounds for Applying

You may apply for a holdover of provisional profits tax on the following grounds:

- Income will be lower: Your assessable profits for the year in question will be less than 90% of the prior year's assessable profits. In other words, your income must fall by more than 10%.

- Objection to prior year: You have lodged a valid objection or appeal against the assessment used as the basis for the provisional tax calculation.

- Cessation of business: You have ceased or are about to cease the trade, profession, or business giving rise to the liability.

For salaries tax, the grounds include situations where your employment income will not exceed HKD 132,000 (the basic allowance threshold), your assessable income will be less than 90% of the prior year, or you have lodged an objection against the underlying assessment.

Timing and Procedure

The holdover application must be lodged at least 28 days before the due date of the first instalment. Missing this deadline is the single most common reason holdover applications are refused, so calendar this well in advance once you receive your demand note.

To apply:

- Profits tax: Submit Form BIR54 to the IRD, setting out the grounds and your estimated assessable profits for the year

- Salaries tax: Submit Form IR1121

Both forms are available on the IRD website. The application should include supporting documentation such as management accounts, projections, or evidence of business changes that justify the expected reduction.

The IRD will review the application and notify you of their decision. If approved, you either pay a reduced amount or defer payment until the actual assessment is raised. If refused, the original instalment dates and amounts stand.

What Happens After Holdover Is Granted

A holdover is not a cancellation. When the IRD raises the actual assessment for the year, any difference between the actual liability and the held-over provisional tax will be payable (or refundable). If your actual profits turn out to be higher than your estimate in the holdover application, the IRD may impose a surcharge on the understated amount, so it pays to be conservative but realistic in your projections.

Penalties for Late Payment

The IRD applies penalties in stages for late or missed provisional tax payments:

| Stage | Penalty |

|---|---|

| Payment not received by due date | 5% surcharge on the outstanding amount |

| Still unpaid 6 months after the original due date | Additional 10% surcharge on the original outstanding amount |

| Continued non-payment | Possible recovery proceedings, including recovery from third parties |

In serious cases, the IRD can apply to the court for a recovery order and attach the debt to property or assets. The total surcharges (5% plus 10%) can be significant on a large provisional tax bill, which is why applying for a holdover well in advance is far preferable to simply not paying.

If you have a genuine cash flow difficulty, speaking with the IRD proactively is advisable. In some circumstances, instalment payment arrangements can be negotiated, although these are not automatic.

For a full calendar of Hong Kong tax deadlines, including provisional tax dates, see our Hong Kong tax deadline checklist.

Provisional Tax vs Final Assessment: How the Offset Works

To illustrate how provisional tax is credited against the final assessment, consider a simplified example:

| Item | Amount (HKD) |

|---|---|

| Provisional profits tax paid (Year 2025/26) | 165,000 |

| Actual assessable profits for 2025/26 | 900,000 |

| Tax at 16.5% (actual assessment) | 148,500 |

| Less: provisional tax already paid | (165,000) |

| Refund due to taxpayer | 16,500 |

In this scenario the business paid slightly more in provisional tax than its actual liability, so the IRD would issue a refund. Had the actual profits been higher, the balance would be payable when the assessment was issued.

For a broader overview of Hong Kong's corporate tax framework, including the two-tiered profits tax rates and available deductions, see our Hong Kong corporate tax guide.

How Air Corporate Can Help

Need help managing your provisional tax obligations? Air Corporate's accounting team prepares provisional tax estimates, files holdover applications, and monitors IRD deadlines on your behalf. Get in touch with us today to take the stress out of tax season.

Air Corporate is a licensed Hong Kong accounting and company formation firm. Our tax professionals work with SMEs, startups, and international companies to ensure that tax payments are planned, provisional tax is challenged where appropriate, and no deadlines are missed. Whether you need a one-off holdover application or ongoing tax compliance support, we can help.

Air Corporate handles your Hong Kong tax filings and compliance from USD 149/year.Get started today