Hong Kong companies and individuals pay profits tax and salaries tax in advance through a system called provisional tax. When your income for the current year is expected to be significantly lower than last year, you can apply to defer or reduce that provisional payment. This is called holding over provisional tax.

This guide covers when you qualify, how the 90% rule works, the application process, and the deadlines you must not miss. For context on how provisional tax fits into the annual tax cycle, see our Hong Kong corporate tax guide. For the step-by-step process of filing the Profits Tax Return that triggers the provisional tax demand, see our Profits Tax Return guide. For a complete walkthrough of how profits tax is calculated, see our profits tax calculation guide.

Highlights of this article

- Provisional tax is an advance payment calculated on the previous year's income. It applies to both profits tax (companies) and salaries tax (individuals).

- You can apply to hold over all or part of your provisional tax if your income this year is expected to be at least 10% lower than last year. This is the 90% rule.

- Applications must be submitted at least 28 days before the provisional tax payment due date, or within 14 days of receiving the tax demand notice, whichever is later.

- You apply using Form IR1121 (paper) or via eTAX (online). You must include supporting documents proving the expected income reduction.

- Holding over delays payment. It does not reduce the final tax owed. Once the IRD issues its final assessment, any remaining balance becomes due.

What provisional tax is

Hong Kong's tax system collects tax in advance through provisional assessments. Instead of paying the full tax bill only when you file your annual return, you pay estimated tax during the year based on the previous year's figures. The IRD then reconciles the provisional payments against the actual liability once the final assessment is issued.

For companies, provisional profits tax is billed together with the final profits tax assessment. A single tax demand covers 2 amounts:

- The final profits tax for the completed year of assessment

- The provisional profits tax for the current year (typically 100% of the preceding year's final liability)

For individuals, provisional salaries tax is split into 2 installments:

- First installment: approximately 75% of the provisional tax, due around January

- Second installment: the remaining 25%, due around April

Example: If provisional salaries tax for the year is HKD 20,000, the IRD typically demands HKD 15,000 in January and HKD 5,000 in April.

Missing the first installment causes the second installment to become immediately due. A 5% surcharge applies to outstanding tax, with further recovery action if payment is not made.

Holdover versus tax relief: key distinction

Holding over provisional tax is not the same as getting a tax reduction or waiver. It is important to understand the difference before applying:

| Tax holdover | Tax relief or reduction | |

|---|---|---|

| Purpose | Delay payment of provisional tax | Reduce the total tax payable |

| Effect on final tax | No reduction. Full amount still owed after final assessment. | Permanent reduction in tax liability |

| Timing | Buys time to pay while income is lower | Lowers the bill permanently |

| Examples | Applying because profits are down this year | Claiming MPF deductions, child allowance, or a government rebate |

If you expect to owe less tax permanently (e.g. because of genuine new deductible expenses), tax relief or objection to the assessment is the appropriate route, not a holdover application.

Who qualifies: the 90% rule

The primary eligibility criterion is the 90% rule. Your estimated income or assessable profits for the current year of assessment must be less than 90% of the figure on which provisional tax was calculated (i.e. last year's income or profits).

In practice: if your net assessable profits for 2024/25 were HKD 500,000, your provisional profits tax for 2025/26 is based on HKD 500,000. To qualify for a holdover, your projected 2025/26 profits must be below HKD 450,000 (less than 90% of HKD 500,000).

The IRD also considers exceptional circumstances outside the 90% rule, including:

- A business downturn or significant drop in revenue

- Cessation or winding down of business

- Change of employment or unpaid leave (for salaries tax)

- New allowances that will significantly reduce net chargeable income

- Loss carryback claims or deductible expenses not reflected in the provisional assessment

You can apply to hold over the full provisional amount or a portion of it, depending on the shortfall between your projected and previous year figures.

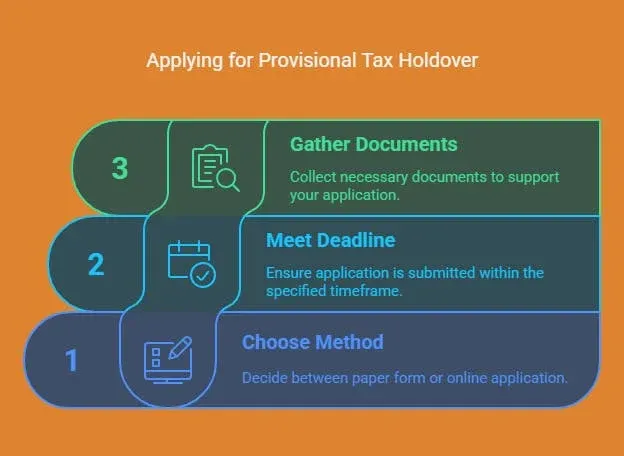

How to apply in 3 steps

Step 1: Check eligibility and gather your supporting documents

Confirm your projected income or profits for the current year fall below 90% of last year's assessed figure. Prepare documents that prove the shortfall:

For companies (profits tax holdover):

- Draft management accounts covering at least 8 months of the current financial year

- Profit and loss statement showing the decline in revenue or profits

- Board resolution or management note explaining the downturn

For individuals (salaries tax holdover):

- Payslips showing salary reduction

- Employer letter confirming reduced salary or unpaid leave

- Termination or redundancy letter (if applicable)

- Medical certificates (if income is reduced due to illness or injury)

Step 2: Submit your application via Form IR1121 or eTAX

There are 2 methods:

Paper: Form IR1121

Download Form IR1121 from the IRD website. Complete your personal or business details, state your estimated income or profits for the current year, and select the grounds for the holdover application. Submit by:

- Mail to: Commissioner of Inland Revenue, P.O. Box 28487, Concorde Road Post Office, Kowloon, Hong Kong

- Fax to: (852) 2519 6896

Ensure all mail carries sufficient postage. Underpaid mail is not accepted by the IRD.

Online: eTAX

If you have an eTAX account with the IRD, log in and navigate to the provisional tax holdover section. Complete the online form and attach scanned supporting documents. You receive an instant acknowledgement on submission. eTAX is available for salaries tax, sole proprietorship profits tax, and property tax.

Step 3: Track your application and confirm outcome

After submission, check your eTAX account for status updates or wait for written confirmation from the IRD by post. If you have not received a response and the payment deadline is approaching, contact the IRD directly to confirm receipt. Do not assume approval. If the IRD rejects the application, the original tax demand remains payable.

Deadlines you must not miss

Your application must be submitted no later than the later of:

- 28 days before the due date for the provisional tax payment

- 14 days after the date of issue of the provisional tax demand notice

Example: If your payment is due on 15 January and the tax demand notice was issued on 1 December, the deadline is 18 December (28 days before 15 January). The 14-day rule (by 15 December) is earlier, so the 28-day rule applies.

If provisional tax is split into 2 installments and you have already paid the first, you can still apply to hold over the second installment, provided you meet the eligibility criteria and submit before the second installment deadline.

Common mistakes when applying

| Mistake | What you need to know |

|---|---|

| Missing the deadline | Applications submitted after the deadline will not be accepted. Calculate the deadline carefully from the tax demand notice. |

| No supporting documents | The IRD will not approve a holdover without evidence of the expected income reduction. Include accounts, payslips, or letters. |

| Income drop under 10% | Minor shortfalls do not qualify under the 90% rule. Only apply if the drop is material. |

| Confusing holdover with tax reduction | A successful holdover does not reduce what you owe. The deferred amount becomes payable after final assessment. |

| Not confirming receipt | If you submit by post, follow up with the IRD to confirm the application was received before the deadline. |

What happens after the holdover is granted

Once the IRD approves the holdover, the deferred amount is suspended. When the IRD issues the final assessment for the current year, it reconciles the actual tax liability against provisional payments already made. If you owe more than you paid, the balance becomes due. If you overpaid (because your actual income turned out to be even lower than projected), the excess is credited against future tax or refunded.

A holdover is not permanent relief. It is a cash flow tool for years where income or profits drop materially.

Your company secretary handles annual statutory filings, but provisional tax holdover applications are an accounting and tax matter. Your accountant or tax representative submits the application on your behalf and monitors the IRD's response. For the full list of annual tax obligations for Hong Kong companies, see our annual requirements guide.

Air Corporate handles audit and tax filing for Hong Kong companies from USD 580/year. This includes profits tax returns, provisional tax management, and IRD correspondence. Get started