Most founders registering a Hong Kong company assume withholding tax will be a major concern. It is not. Hong Kong imposes no withholding tax on dividends and no withholding tax on interest. The system is one of the most straightforward in Asia.

Withholding tax in Hong Kong applies in only 2 situations: royalties paid to non-residents for intellectual property used in Hong Kong, and fees paid to non-resident entertainers and sportspeople for performances in Hong Kong. Everything else is outside scope.

This guide covers exactly when withholding tax applies, the rates, how Double Taxation Agreements (DTAs) reduce liability, and the compliance steps required. For the broader tax picture, see our Hong Kong corporate tax guide.

Highlights of this article

- Hong Kong imposes no withholding tax on dividends paid to non-resident shareholders.

- Hong Kong imposes no withholding tax on interest payments to non-residents.

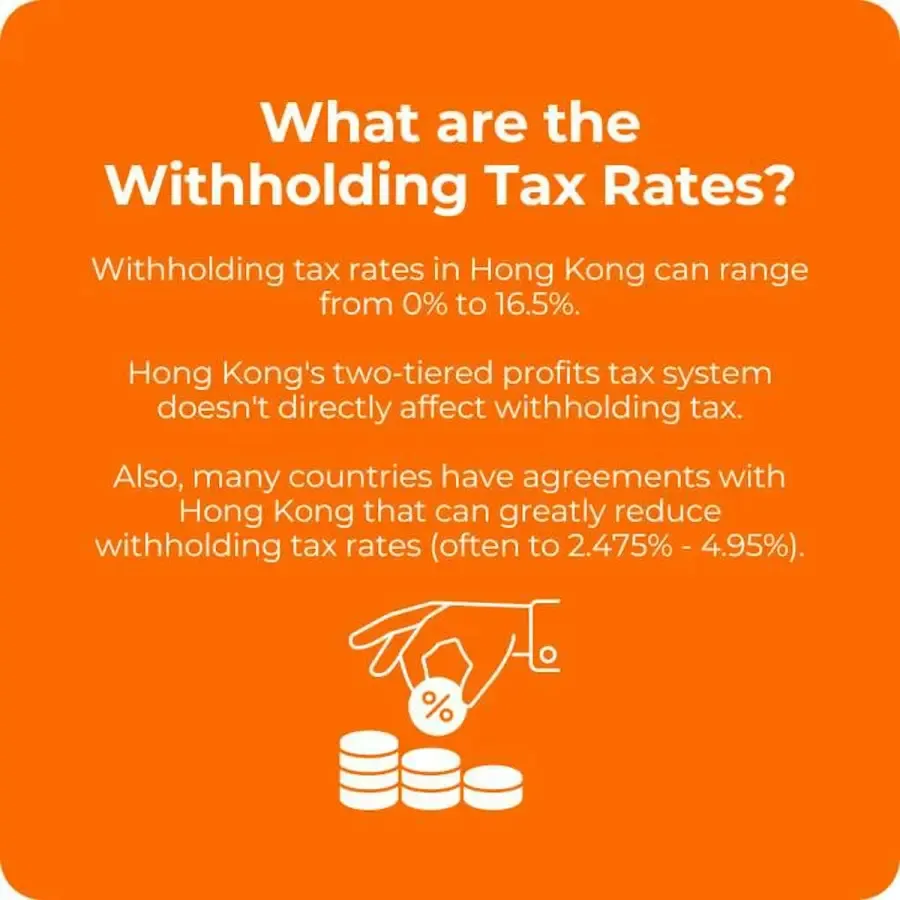

- Withholding tax applies to royalties paid to non-residents: 4.95% for non-associates, 16.5% for associates (IP previously owned by the payer in Hong Kong).

- Fees for non-resident entertainers and sportspeople performing in Hong Kong are subject to 10% withholding (11% if paid through an agent).

- Hong Kong has signed DTAs with 50+ jurisdictions. Under most treaties, royalty withholding tax is reduced to 2.475% to 4.95%.

- The payer (the Hong Kong company) is responsible for withholding, remitting, and reporting to the IRD.

What withholding tax means in Hong Kong

Withholding tax is a mechanism where the payer deducts tax at source before remitting funds to the recipient. The deducted amount is paid directly to the Inland Revenue Department (IRD) on behalf of the non-resident recipient.

The key point for Hong Kong companies is scope. Unlike most jurisdictions, Hong Kong's withholding tax regime is deliberately narrow. It targets only specific passive income flowing to non-residents, not general commercial payments.

A Hong Kong company paying a foreign supplier for services performed outside Hong Kong does not trigger any withholding obligation. A Hong Kong company paying dividends to overseas shareholders triggers no withholding. The tax applies when specific criteria are met, not as a default on outbound payments.

Income NOT subject to withholding tax

Most outbound payments from Hong Kong companies carry zero withholding tax:

| Payment type | Withholding tax |

|---|---|

| Dividends to non-resident shareholders | 0% |

| Interest to non-resident lenders | 0% (in most cases) |

| Service fees for work performed outside Hong Kong | 0% |

| Capital gains distributions | 0% |

| Loan repayments | 0% |

| Rental income (paid to non-residents) | 0% |

The absence of dividend withholding tax is one of the most significant advantages of the Hong Kong structure for foreign founders. Profits can be distributed to shareholders anywhere in the world without any Hong Kong-level deduction. For a detailed breakdown of how dividends are taxed, see our guide to dividend income in Hong Kong.

The 2 situations where withholding tax applies

Royalties paid to non-residents for IP used in Hong Kong

When a Hong Kong company pays royalties to a non-resident for the use of intellectual property in Hong Kong, withholding tax applies. The rate depends on whether the payer and recipient are associates and whether the IP was previously owned by the payer.

Non-associate rate (standard):

The withholding tax is calculated as 4.95% of the gross royalty amount. This is derived from applying the 16.5% profits tax rate to 30% of the royalty (30% × 16.5% = 4.95%). The IRD treats 30% of the royalty as the notional profit from licensing.

Associate rate (IP previously owned by the payer):

If the IP was at any time owned by the Hong Kong payer and then transferred to the non-resident licensor, a higher rate applies. The withholding tax is 16.5% of the gross royalty (i.e., 100% of the royalty is treated as profit). This anti-avoidance rule prevents companies from stripping profits offshore via related-party IP transfers.

| Royalty recipient | Relationship | Rate |

|---|---|---|

| Non-resident company | Non-associate | 4.95% of gross royalty |

| Non-resident company | Associate (IP previously in HK) | 16.5% of gross royalty |

| Non-resident individual | Non-associate | 4.5% of gross royalty |

| Non-resident individual | Associate (IP previously in HK) | 15% of gross royalty |

IP types subject to this withholding: patents, copyrights, trademarks, registered designs, know-how, and similar rights.

Fees for non-resident entertainers and sportspeople

When a Hong Kong company or promoter pays a non-resident entertainer, performer, or sportsperson for activities carried out in Hong Kong, withholding tax applies.

| Payment structure | Rate |

|---|---|

| Paid directly to the non-resident performer | 10% of gross payment |

| Paid through an agent or management company | 11% of gross payment |

This covers concerts, sporting events, television appearances, and similar engagements performed physically in Hong Kong. Fees for work performed outside Hong Kong are not subject to this withholding.

How DTA relief reduces withholding tax

Hong Kong has signed Comprehensive Double Taxation Agreements (CDTAs) with over 50 jurisdictions. Under most CDTAs, the withholding tax rate on royalties is reduced significantly.

Common treaty rates on royalties:

| Treaty partner | Standard rate | DTA rate |

|---|---|---|

| United Kingdom | 4.95% | 3% |

| Germany | 4.95% | 3% |

| France | 4.95% | 3% |

| Singapore | 4.95% | 3% |

| Australia | 4.95% | 5% |

| China (Mainland) | 4.95% | 7% |

| Netherlands | 4.95% | 3% |

Under the most favourable treaties, the rate can fall as low as 2.475% on royalties where the payer is an associate but the IP was not previously held in Hong Kong.

To claim DTA relief, the recipient must demonstrate tax residency in the treaty partner jurisdiction. For individuals, this means residing in the treaty country for at least 180 days per year. For companies, it means being incorporated or centrally managed in the treaty country.

For the full list of Hong Kong's DTA network and how treaty relief is claimed, see our double taxation agreements guide.

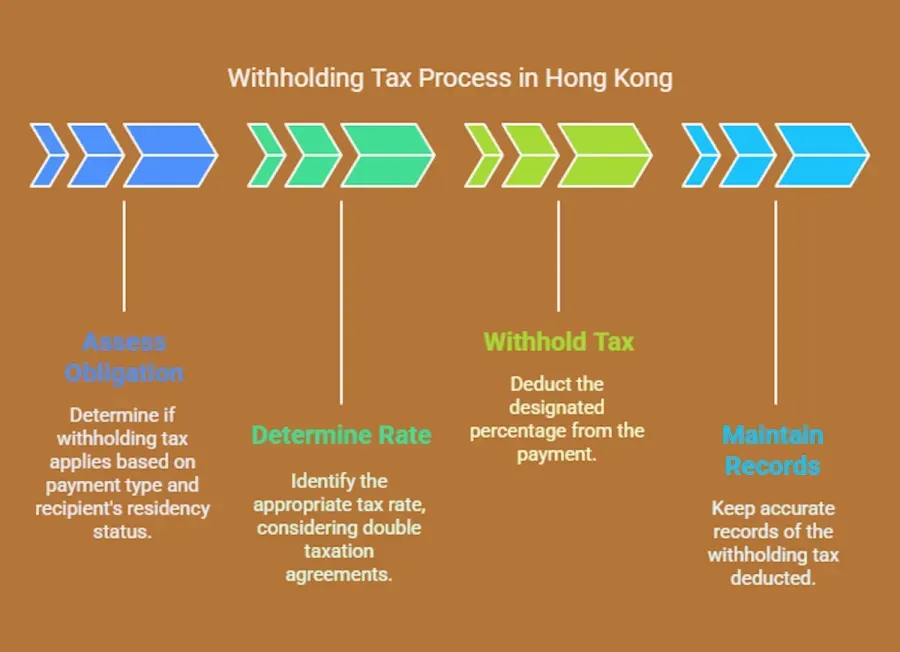

How to comply: withholding tax in 4 steps

Step 1: Determine whether withholding tax applies

Review the nature of the payment. If it is a royalty for IP used in Hong Kong, or a fee for entertainment or sports performed in Hong Kong, withholding obligations exist. If it is a dividend, interest, or service fee for work performed outside Hong Kong, no withholding applies.

Step 2: Calculate the correct rate

Identify whether the recipient is a non-associate or associate. Check whether any DTA applies by confirming the recipient's tax residency in a treaty jurisdiction. Apply the correct rate to the gross payment before remittance.

Step 3: Withhold the amount and remit to the IRD

Deduct the withholding tax from the payment before transferring to the non-resident. Remit the withheld amount to the IRD. Timing requirements vary: royalty withholding obligations arise at the time of payment or credit, whichever is earlier.

Step 4: File the required returns and maintain records

File the appropriate return with the IRD. Maintain records of all withholding calculations, payments, and DTA claims for a minimum of 7 years. The IRD may audit withholding tax compliance as part of a profits tax field audit.

What happens if you fail to withhold

If a Hong Kong company fails to withhold when required, the IRD holds the payer liable for the unpaid tax plus interest and penalties. The withholding obligation does not transfer to the non-resident recipient. This makes it critical to assess every outbound royalty or entertainer payment for withholding implications before transfer.

Your company secretary does not handle withholding tax filings. This is an accounting and tax matter handled by your accountant or tax representative.

Air Corporate handles annual audit and tax filing for Hong Kong companies from USD 580/year. This includes profits tax returns, IRD correspondence, and advice on withholding obligations. Get started