Every Hong Kong company that pays salaries, fees, or benefits to any person must file an Employer's Return with the Inland Revenue Department each year. This is not optional, even if you have no employees or your business is dormant. If you receive Form BIR56A from the IRD, you must return it.

This guide covers who must be reported, which forms to use, what income to declare, the deadlines for each scenario, and how to file. For the full list of annual tax obligations for Hong Kong companies, see our annual requirements guide.

Highlights of this article

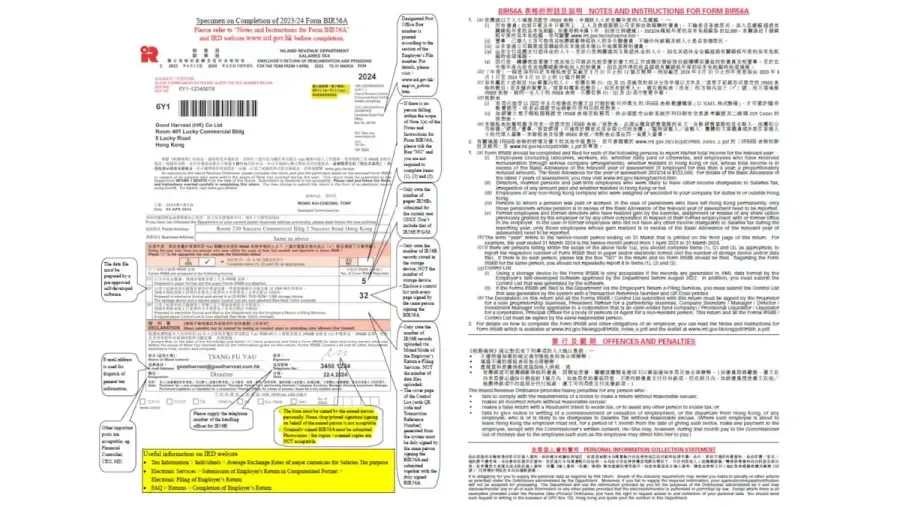

- The Employer's Return (Form BIR56A) is issued by the IRD around 1 April each year and must be filed within 1 month of issue, typically by early May.

- One Form IR56B must accompany BIR56A for each reportable person. The income threshold for 2024/25 is HKD 132,000 per person. Directors are always reportable regardless of amount.

- Storage devices are no longer accepted for electronic IR56B submissions from 1 April 2024. Use the IRD's Employer's Return e-Filing Services (online or Mixed Mode only).

- Separate forms apply when employees start (IR56E), leave or pass away (IR56F), or permanently leave Hong Kong (IR56G).

- Payroll records must be kept for at least 7 years. Failure to file or incorrect returns can result in prosecution, additional tax assessments, and heavy fines.

What the Employer's Return covers

The Employer's Return (Form BIR56A) is the annual return of remuneration and pensions paid to employees and other reportable persons during the year from 1 April to 31 March.

BIR56A is the cover form. It is submitted together with one IR56B for each reportable person. BIR56A states the number of IR56B forms attached and is signed by an authorised signer: a director, company secretary, manager, or precedent partner for a corporation.

If you receive BIR56A but have no one to report, tick "NO" on the form and still return BIR56A to the IRD. If you did not receive BIR56A by mid-April, request a duplicate through the IRD's eTAX portal or the Fax-A-Form service.

Who counts as a reportable person

For IRD purposes, "employee" is broadly defined. A reportable person includes:

- Any person you engage, whether resident or non-resident, for work in Hong Kong or overseas

- Directors (regardless of the amount paid, if they are likely to have other chargeable income)

- Married persons

- Part-time employees likely to have other chargeable income

- Employees of non-Hong Kong entities seconded or assigned to you for duties in or outside Hong Kong

- Pensioners to whom you paid or accrued a pension

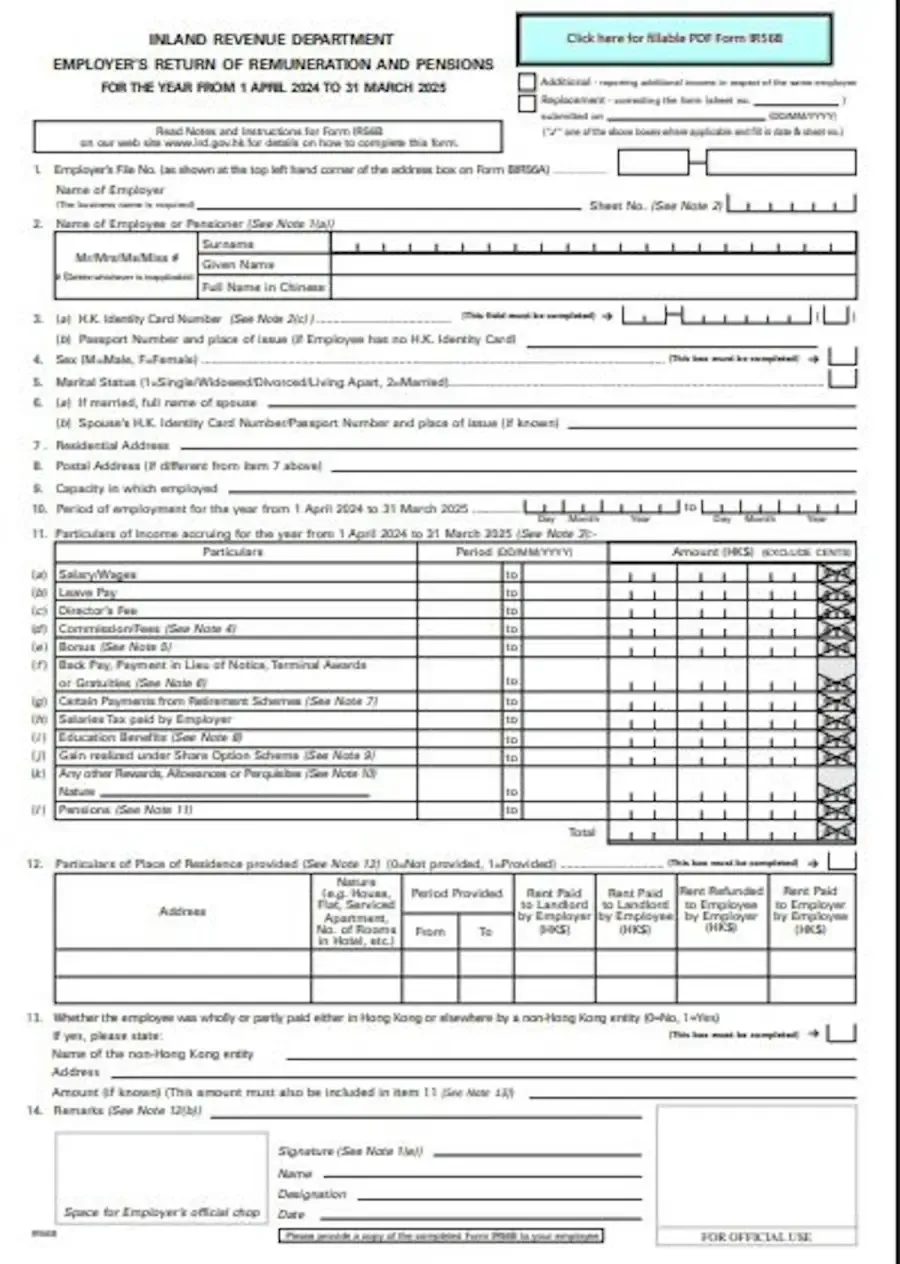

When IR56B is required

You must file IR56B for a reportable person if:

- Their total income for the year exceeds the Basic Allowance: HKD 132,000 for 2024/25 (pro-rated if employed for only part of the year)

- They are a director, married person, or part-time employee likely to have other chargeable income, regardless of the amount paid

Do not file IR56B for any person for whom you have already filed IR56F (cessation) or IR56G (permanent departure from Hong Kong) for the same year of assessment.

What income to report on IR56B

Form IR56B must capture all chargeable income, not just basic salary:

| Income type | Reportable |

|---|---|

| Salary, wages, bonuses, commissions | Yes |

| Leave pay and gratuities | Yes |

| Director's fees | Yes |

| Payments in lieu of notice (from 1 April 2012 onwards) | Yes |

| Allowances and perquisites | Yes |

| Value of employer-provided housing | Yes |

| Holiday journey benefits | Yes |

| Stock awards and share options | Yes |

| Employer-paid tax | Yes |

| Pension payments and retirement scheme payouts | Yes. Subject to Basic Allowance test if person has left HK permanently. |

| Income paid by a non-Hong Kong entity on your behalf | Yes |

Report gross income, not net pay. Under-reporting benefits such as housing or share awards is one of the most common compliance errors.

Freelancers: Form IR56M and IR6036B

If you pay local persons who are not your employees, a separate form applies. File Form IR56M together with Form IR6036B when annual payments to a single person exceed:

- HKD 25,000 for consultants, agents, or freelancers

- HKD 200,000 for sub-contractors

These thresholds apply to the year of assessment (1 April to 31 March). Give a copy of the filed IR56M to the recipient to help them complete their own tax return.

Filing deadlines for all IR56 forms

| Form | Trigger | Deadline |

|---|---|---|

| BIR56A + IR56B | Annual issue by IRD (around 1 April) | Within 1 month of issue |

| IR56E | New employee hired | Within 3 months of hire date |

| IR56F | Employee ceases employment or passes away | Not later than 1 month before cessation date |

| IR56G | Employee leaving Hong Kong permanently | At least 1 month before departure date |

| IR56M + IR6036B | Payments to freelancers/sub-contractors | Filed with the annual BIR56A |

For IR56F and IR56G, do not also file IR56B for the same period. One form per trigger event per person.

For IR56G (permanent departure), you are required to withhold sufficient money from the employee to cover any outstanding tax liability. The employee must obtain a tax clearance letter from the IRD before leaving. Do not release all final payment until clearance is obtained.

You may apply in writing to the IRD for an extension of time to file BIR56A if needed.

How to file

Step 1: Receive BIR56A and verify the details

The IRD issues Form BIR56A around 1 April each year. When it arrives, confirm the company name, business registration number, and the period of the return (1 April to 31 March). If you did not receive BIR56A by mid-April, request a duplicate through the IRD's eTAX portal or the Fax-A-Form service. You cannot simply skip filing because the form did not arrive. Requesting a duplicate is your obligation.

Step 2: Compile income data for all reportable persons

Gather complete payroll data for every person who received remuneration during the year. This includes salary, bonuses, commissions, director's fees, benefits in kind (housing, car, club memberships), stock awards, and holiday journey benefits. Report gross income, not net pay. For each person, check whether their total income exceeds the HKD 132,000 threshold, or whether they are a director, married person, or part-time employee who must be reported regardless of amount.

Step 3: Complete one IR56B for each reportable person

Prepare Form IR56B for every person who meets the reporting criteria. IR56B captures the individual's name, Hong Kong Identity Card number, total income for the year, and a breakdown by income type. Do not round down or omit benefits. Under-reporting benefits such as housing values and share awards is one of the most common compliance errors and can lead to back assessments and penalties. Provide a copy of each completed IR56B to the relevant person before filing.

Step 4: File using paper, eTAX, or Mixed Mode

Paper filing: Download BIR56A and IR56B from the IRD website, complete them, and submit with original wet-ink signatures. Photocopies and scans are not accepted.

Online filing via eTAX: Log in and use the Employer's Return e-Filing Services to submit BIR56A, IR56B, IR56E/F/G, and IR6036B/IR56M electronically. This is the most efficient method for most companies. From 1 April 2024, the IRD no longer accepts IR56B records submitted via removable storage devices (USB drives, CDs). All electronic IR56B submissions must go through the e-Filing Services.

Mixed Mode filing: A designated person uploads the IR56B data file to the IRD system without the authorised signer's login credentials. The system generates a Control List with a Transaction Reference Number and QR code. The authorised signer then signs the Control List cover page and submits it to the IRD together with BIR56A to complete the filing.

Step 5: Retain all records for 7 years

After filing, retain a complete copy of BIR56A, all IR56B forms, and all supporting payroll records for at least 7 years. The IRD can request these records at any time. If a reportable person disputes the income figure on their IR56B with the IRD, your records are your primary evidence. Payroll records must be detailed enough to reconstruct the income figure for any individual in any month of the assessment year.

Common mistakes to avoid

| Mistake | What you need to know |

|---|---|

| Reporting net pay instead of gross | Always report gross income including all benefits and allowances |

| Omitting housing or share award values | These are chargeable income and must appear on IR56B |

| Filing IR56B after already filing IR56F/G | File only 1 form per person per event. Do not duplicate. |

| Missing IR56E for new hires | IR56E must be filed within 3 months of hiring, not just at year-end |

| Releasing final pay before IR56G clearance | Withhold until IRD issues tax clearance for employees leaving HK permanently |

| Not giving the reportable person a copy | The person must receive a copy of their IR56 form for their own tax return |

| Payroll records under 7 years | IRD requires records for at least 7 years |

Penalties for non-compliance

Failure to file the Employer's Return or filing an incorrect return can result in:

- Prosecution under the Inland Revenue Ordinance

- Additional tax assessments against the employer

- Heavy fines

The IRD treats the Employer's Return as a mandatory obligation. Late or missing BIR56A submissions are flagged for follow-up. Employers with a history of late filing may face increased scrutiny in subsequent years.

Specific penalties under the Inland Revenue Ordinance include:

| Breach | Penalty |

|---|---|

| Failure to file BIR56A | Fine up to HKD 10,000 + additional tax assessment |

| Filing incorrect IR56B | Fine up to HKD 10,000 per incorrect form |

| Failure to file IR56E/F/G on time | Fine up to HKD 10,000 |

| Wilful intent to evade tax | Prosecution, fine up to 3 times the tax undercharged, and imprisonment |

Note that incorrect IR56B filings affect the employee directly. The IRD uses IR56B data to issue the Salaries Tax Return to each individual. If you under-report an employee's income, the employee's Salaries Tax assessment will be wrong. The IRD will correct it when the error is discovered, which can create a backdated liability for the employee and an investigation into the employer.

Employer obligations for new and departing employees

The Employer's Return is an annual obligation, but 3 IR56 forms have event-specific triggers throughout the year:

IR56E: New employee notification. File within 3 months of the employment start date for any new employee who is likely to have total income exceeding the Basic Allowance. Do not wait for the annual cycle. If a new hire starts in June and their income will clearly exceed HKD 132,000 for the year, IR56E should be filed by September.

IR56F: Employee cessation. File at least 1 month before the employee's last day of employment, or promptly if the cessation is unexpected (such as a sudden resignation or death). IR56F reports the final period's income and triggers the IRD to issue a tax demand to the individual. Do not also file IR56B for the same period.

IR56G: Permanent departure from Hong Kong. File at least 1 month before the employee's departure date. You must withhold sufficient final payment to cover any outstanding tax. The employee must obtain a tax clearance letter from the IRD before you release the withheld funds. This protects you from liability if the employee leaves with unpaid tax.

Your company secretary does not prepare or file the Employer's Return. This is an accounting and payroll obligation managed by your accountant or payroll provider. For the full corporate tax picture, see our Hong Kong corporate tax guide.

Air Corporate handles accounting and bookkeeping for Hong Kong companies from USD 95/month. Get started