When Can You Actually Access Your MPF Savings?

You have been contributing to your Mandatory Provident Fund (MPF) account for years, watching the balance grow on your statements. But the rules around when and how you can actually get that money back are not always obvious. Many Hong Kong employees are surprised to discover the conditions are stricter than they expected, while others miss legitimate withdrawal opportunities they did not know existed.

This guide covers every valid MPF withdrawal scenario, the exact forms to file, typical processing times, and what happens to your money from a tax perspective.

Key Highlights

- You can withdraw your full MPF balance at age 65, or early retirement from age 60 if you permanently cease employment

- Non-residents leaving Hong Kong permanently can make a one-time full withdrawal regardless of age

- Total incapacity and terminal illness qualify for early withdrawal

- MPF withdrawals are not subject to salaries tax in Hong Kong

- Since January 2016, members aged 65 and above can receive benefits in phased instalments rather than a lump sum

- Voluntary contributions and mandatory contributions follow different withdrawal rules

What Is the MPF Scheme?

The Mandatory Provident Fund is Hong Kong's compulsory retirement savings system, established under the Mandatory Provident Fund Schemes Ordinance (Cap. 485), which came into force on 1 December 2000. Both employers and employees contribute 5% of the employee's relevant income (capped at HKD 1,500 per month each based on a maximum relevant income of HKD 30,000 per month) to an MPF scheme managed by a registered trustee.

There are currently around 23 registered MPF trustees overseeing hundreds of constituent funds. Your contributions are invested in these funds and accumulate as "accrued benefits" until a valid withdrawal event occurs.

For a deeper overview of how the scheme operates, see our guide on MPF in Hong Kong and MPF contribution amounts and calculations.

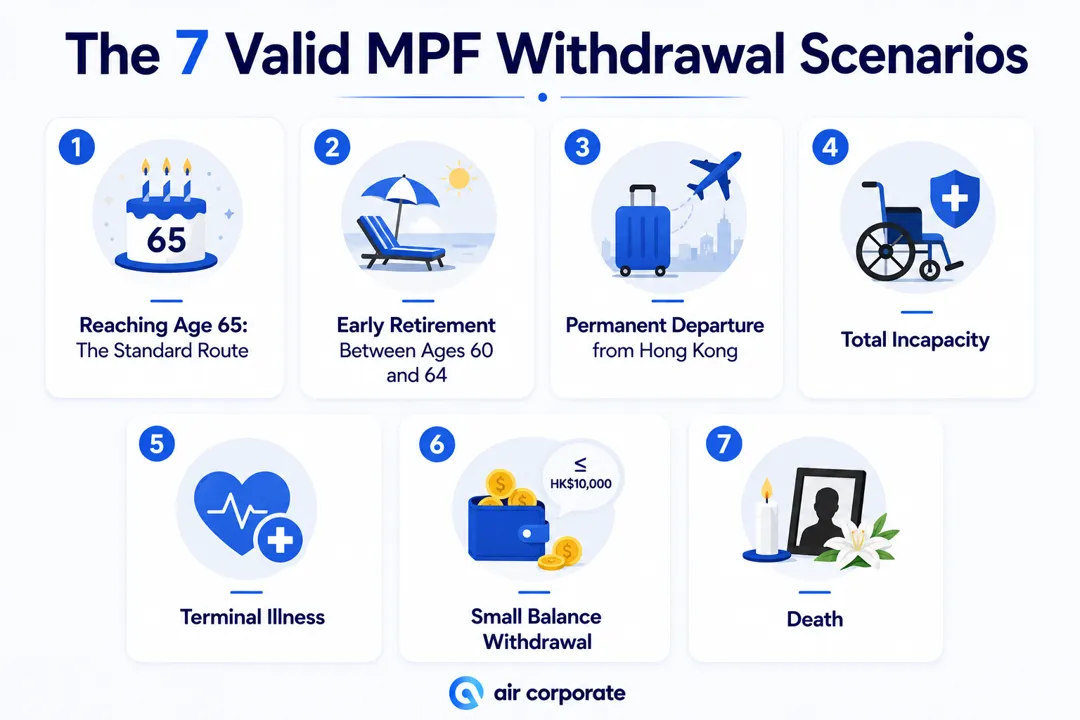

The 7 Valid MPF Withdrawal Scenarios

1. Reaching Age 65: The Standard Route

The primary withdrawal trigger is reaching age 65. At this point, you are entitled to withdraw your full accrued benefits from all MPF accounts, regardless of whether you are still working. You do not need to retire to access your savings once you turn 65.

The trustee will require proof of age (typically a copy of your Hong Kong Identity Card or passport) along with the standard withdrawal form.

2. Early Retirement Between Ages 60 and 64

If you are between 60 and 64 and you permanently cease all employment and self-employment, you can apply for early withdrawal. The key word is "permanently." You cannot plan to return to work later and still qualify. Most trustees will ask you to sign a statutory declaration confirming your permanent retirement from the workforce.

If you later resume employment after an early withdrawal, you will need to rejoin an MPF scheme through your new employer, and contributions will restart from zero.

3. Permanent Departure from Hong Kong

Non-permanent residents (and permanent residents) who are leaving Hong Kong permanently and have no intention of returning to live or work can apply for a one-time full withdrawal of their accrued benefits. This applies regardless of age.

This is a one-time option. Once you make the claim, the trustee closes your account. If you later return to Hong Kong and take up employment, you will need to enrol in a new MPF scheme. You cannot "undo" the permanent departure withdrawal.

The relevant form for this scenario is Form MPF(S)(P). You will need to provide evidence of your departure (such as a one-way exit permit or documentation of permanent residency status abroad).

4. Total Incapacity

Members who are permanently unable to work due to a physical or mental disability can withdraw their full accrued benefits regardless of age. A registered medical practitioner must certify that the disability is permanent and that the member is permanently unfit for any work.

This is a high threshold. A temporary injury or illness, even a serious one, does not qualify. The disability must be permanent and total.

5. Terminal Illness

If a registered medical practitioner certifies that a member has less than 12 months to live, an early full withdrawal is permitted. This allows terminally ill members to access their savings for medical care, family support, or estate planning purposes.

6. Small Balance Withdrawal

This is the least-known legitimate withdrawal route. If a former employer's account (not the current employer's account) has an accrued balance of HKD 5,000 or less, AND no contributions have been made to that account for 12 months or more, the member can apply to withdraw the full balance.

Note that this applies only to accounts from former employers, not the current employer's scheme. This provision helps members clean up dormant small accounts that have accumulated over many job changes.

7. Death

Upon the death of an MPF member, the accrued benefits are paid to the deceased member's legal personal representative (executor or administrator of the estate). The benefits form part of the estate and are distributed according to the member's will or the rules of intestacy if there is no will.

Trustees typically require a grant of probate or letters of administration before releasing funds.

What Does NOT Qualify for MPF Withdrawal

One of the most common misconceptions is that redundancy, layoff, or financial hardship entitles you to withdraw your MPF. It does not. If you are made redundant, you may be entitled to a severance payment from your employer, but your MPF balance remains locked unless one of the seven triggers above applies.

Similarly, purchasing a home, paying for education, or other financial needs do not qualify as withdrawal events. The scheme is designed specifically as a retirement safety net.

Partial withdrawals are also generally not permitted, except in some voluntary contribution arrangements (discussed below). The withdrawal of mandatory contributions is almost always all-or-nothing once a qualifying event occurs.

Voluntary Contributions: A More Flexible Layer

Many MPF schemes allow members and employers to make voluntary contributions on top of the mandatory 5% contributions. These voluntary contribution accounts often have more flexible withdrawal terms, depending on the specific scheme rules set by the trustee.

Some voluntary contribution accounts allow withdrawal at any time, others tie them to the same triggers as mandatory contributions, and some have vesting schedules (where employer voluntary contributions only become the employee's property after a certain number of years of service). You should check your specific MPF scheme's governing rules or ask your HR department for details.

This distinction matters: when people say "I can withdraw my MPF contributions," they often mean only the voluntary portion.

How to Apply for MPF Withdrawal

| Withdrawal Reason | Primary Form | Key Supporting Documents |

|---|---|---|

| Age 65 / Early retirement (60 to 64) | Form MPF(W) | HKID or passport, proof of age, statutory declaration (early retirement) |

| Permanent departure from HK | Form MPF(S)(P) | Exit permit, proof of overseas residency or settlement |

| Total incapacity | Form MPF(W) | Medical certificate from registered practitioner |

| Terminal illness | Form MPF(W) | Medical certificate (less than 12 months prognosis) |

| Small balance | Form MPF(W) | Account statement showing balance and inactivity |

| Death (estate claim) | Trustee-specific forms | Grant of probate or letters of administration |

The standard withdrawal application form is Form MPF(W), available from your MPF trustee's website or branches. Some trustees have digitised this process, allowing online or mobile app submission.

Once you submit your application with all required documents, the trustee typically processes the claim within 30 working days. Some trustees are faster, particularly for straightforward age-65 claims.

Phased Drawdown Option for Age 65 and Above

Since January 2016, members who have reached age 65 are no longer required to take their accrued benefits as a single lump sum. You can instead elect to receive the benefits in regular instalments over time, a structure similar to an annuity.

This option gives retirees more control over cash flow and can be useful for budgeting purposes. You specify the instalment schedule (monthly, quarterly, etc.) and the amount or duration. Your remaining balance continues to be invested in your chosen MPF funds during the drawdown period, meaning it can continue to grow (or fluctuate) in value.

Not all trustees offer the same flexibility with phased drawdown, so it is worth comparing options before you reach retirement age.

Industry Schemes: Construction and Catering Sectors

Workers in Hong Kong's construction and catering industries are covered by special Industry Schemes rather than the standard employer-linked schemes. These sectors have high employee mobility, with workers frequently changing worksites or employers.

Under Industry Schemes, benefits are portable: contributions follow the individual worker regardless of which employer or site they are working at. The withdrawal conditions are the same as for standard MPF schemes, but the portability structure means workers in these industries do not accumulate fragmented accounts in the same way as other employees.

Tax Treatment of MPF Withdrawals

This is one of the most reassuring aspects of the MPF system: accrued benefits (both mandatory and voluntary contributions, plus investment returns) are NOT subject to salaries tax upon withdrawal. The Inland Revenue Ordinance specifically exempts MPF accrued benefits from salaries tax.

This applies to all withdrawal scenarios: retirement at 65, early retirement, permanent departure, incapacity, and all others. The tax-exempt status is one of the key advantages of building savings through MPF versus other savings vehicles.

For more on how salaries tax works in Hong Kong, see our guide to Hong Kong salaries tax.

MPF and Other Employee Termination Benefits

It is important to understand how MPF interacts with other payments you may receive upon leaving employment. If you are dismissed after two or more years of continuous service, you may be entitled to a severance payment from your employer. If you resign after five or more years, you may be entitled to a long service payment.

Historically, employers could offset severance and long service payment obligations using their MPF employer contributions. However, this offsetting arrangement was abolished with effect from 1 May 2025. For details on this significant change, see our article on severance payments in Hong Kong and long service payments.

The key point: your MPF savings and any severance or long service payment you are entitled to are now separate. Receiving a severance or long service payment does not reduce your MPF accrued benefits.

Need help with your company's ongoing compliance? Air Corporate provides company secretary, accounting, and tax filing services for Hong Kong companies. Speak to our team.