A Major Change to Hong Kong Employment Law Is Already in Effect

On 1 May 2025, one of the most significant changes to Hong Kong's employment benefits framework in decades took effect. The MPF offsetting arrangement, which allowed employers to use their Mandatory Provident Fund contributions to offset severance payment and long service payment obligations, was abolished.

If you employ staff in Hong Kong and have not yet reviewed your liability provisions or employment agreements, this change has direct financial consequences for your business. This guide explains exactly what changed, what remains the same, and what you need to do now.

Key Highlights

- The MPF offsetting arrangement was abolished with effect from 1 May 2025 under the Employment and Retirement Schemes Legislation (Offsetting Arrangement) (Amendment) Ordinance 2022

- Employer MPF contributions made after 1 May 2025 can no longer be used to offset severance payment (SP) or long service payment (LSP) obligations

- Employer MPF contributions accumulated before 1 May 2025 are "grandfathered" and can still be used for offsetting (the pre-enactment portion)

- Employee MPF contributions were never usable for offsetting and remain unchanged

- A government subsidy scheme exists to help qualifying SMEs manage the increased cost burden

- No changes have been made to the calculation formula for SP or LSP, only the offset mechanism is gone

What Was MPF Offsetting?

When the MPF scheme launched in December 2000, the government included a transitional provision allowing employers to offset their severance payment and long service payment obligations using the employer's MPF contributions. The logic was that both MPF contributions and SP/LSP serve a similar retirement-income-replacement purpose, so double-payment seemed like an unintended windfall.

In practice, this meant that an employer who owed an employee a sizeable severance payment could deduct the accumulated value of all employer MPF contributions from the amount owed. For long-tenured employees, this offset could eliminate almost the entire SP/LSP obligation.

For a full explanation of how SP and LSP are calculated, see our articles on severance payments in Hong Kong and long service payments.

The 2022 Ordinance and the 1 May 2025 Commencement Date

The Legislative Council passed the Employment and Retirement Schemes Legislation (Offsetting Arrangement) (Amendment) Ordinance 2022 in June 2022. However, the effective date for the abolition was set as 1 May 2025, giving businesses approximately three years to prepare and adjust their financial provisions.

As of 1 May 2025, the offsetting mechanism for post-enactment employer MPF contributions is gone. Any employer contribution credited to an employee's MPF account from that date forward cannot be used to reduce SP or LSP obligations.

The Pre-Enactment / Post-Enactment Split: What Gets Grandfathered?

The most technically important aspect of the new regime is the distinction between pre-enactment and post-enactment employer MPF contributions.

| Contribution Type | Period | Can be used for SP/LSP offset? |

|---|---|---|

| Employer mandatory contributions | Before 1 May 2025 | Yes (grandfathered, up to value as of 30 April 2025) |

| Employer mandatory contributions | From 1 May 2025 onward | No |

| Employer voluntary contributions | Any period | Subject to scheme rules (generally no, unless specifically structured) |

| Employee mandatory contributions | Any period | Never been usable for offset |

| Employee voluntary contributions | Any period | Never been usable for offset |

The grandfathered amount is the accrued value of employer contributions as of 30 April 2025, including investment gains or losses on those contributions up to that date. This figure is frozen at the 30 April 2025 snapshot. Importantly, investment returns on the pre-enactment contributions after 1 May 2025 are NOT added to the offsettable amount.

Trustees are required to separately track and report the pre-enactment and post-enactment portions of employer contributions. When an employer eventually makes an offsetting claim (against an SP or LSP obligation), the trustee will confirm how much of the pre-enactment amount remains available.

A Worked Example: The Real Financial Impact

Consider an employee who joined a company in January 2017 and is dismissed in December 2026 after approximately 10 years of service. Monthly salary at dismissal: HKD 30,000.

Severance Payment Calculation (unchanged)

SP = Last monthly salary x (2/3) x years of service (capped at HKD 390,000)

SP = HKD 30,000 x (2/3) x 10 = HKD 200,000

Employer MPF Contributions

Monthly employer contribution: 5% x HKD 30,000 = HKD 1,500 per month (ignoring investment returns for simplicity)

Pre-enactment period: January 2017 to April 2025 = 100 months x HKD 1,500 = HKD 150,000 (frozen value as of 30 April 2025)

Post-enactment period: May 2025 to December 2026 = 20 months x HKD 1,500 = HKD 30,000 (cannot be used for offset)

SP Net Cost Under Old Regime (pre-May 2025 rules)

Total employer MPF contributions: approx HKD 180,000

Net SP cost: HKD 200,000 minus HKD 180,000 = HKD 20,000 (employer pays only HKD 20,000 out of pocket)

SP Net Cost Under New Regime

Only pre-enactment contributions (HKD 150,000) remain offsettable

Net SP cost: HKD 200,000 minus HKD 150,000 = HKD 50,000

In this example, the abolition roughly increases the employer's out-of-pocket SP cost from HKD 20,000 to HKD 50,000. For employees with longer tenure hired before 2025, the impact grows substantially because the non-offsettable post-enactment contribution pool expands every year.

Impact on Long-Tenured Employees

The financial impact is most significant for employees who were already working for you before May 2025 and continue to accumulate service afterward. As time passes, a greater proportion of their total employer MPF contributions fall into the non-offsettable post-enactment category.

For employees hired entirely after 1 May 2025, there are no grandfathered contributions at all. The employer cannot offset any portion of SP or LSP against their MPF contributions.

For employees who were already with a company and have long tenures, the grandfathered amount as of 30 April 2025 provides some cushion, but that cushion shrinks in relative terms each passing year.

The Government SME Subsidy Scheme

Recognising the financial burden on smaller businesses, the government established a Subsidy Scheme specifically to help qualifying SMEs transition to the new regime. The scheme provides a tiered government subsidy to eligible employers over a 25-year transitional period.

| Criterion | Threshold for SME eligibility |

|---|---|

| Number of employees | 200 or fewer employees |

| Annual turnover | HKD 400 million or less |

The subsidy works on a tiered basis. For the first 25 years of the transitional period (2025 to 2049), eligible employers receive government subsidies proportional to the additional SP/LSP costs they bear due to the abolition of offsetting. The subsidy percentage decreases over time as the expectation is that businesses will have adjusted their cost structures.

To apply for the subsidy, employers must register through the Labour Department's designated platform and submit claims when SP or LSP payments are made. Documentation of the SP/LSP paid and the corresponding post-enactment MPF contributions is required.

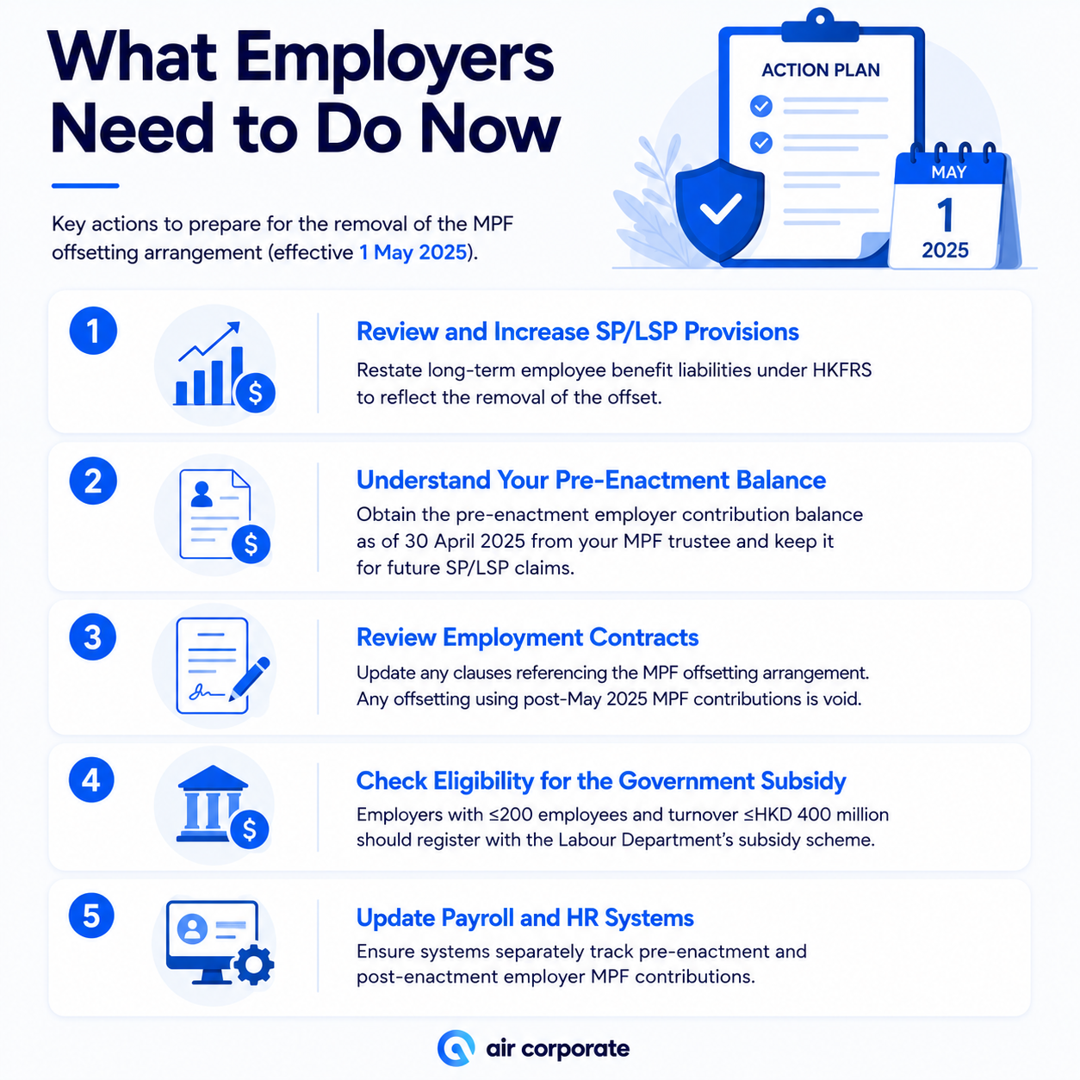

What Employers Need to Do Now

1. Review and Increase SP/LSP Provisions

If your company has made accounting provisions for SP/LSP liabilities assuming the old offsetting arrangement, those provisions are likely understated. Your auditors may require you to restate your long-term employee benefit liabilities under HKFRS (Hong Kong Financial Reporting Standards) to reflect the removal of the offset.

For companies with large workforces of long-tenured employees, this could represent a material change to reported liabilities. Speak to your auditor or accountant about the accounting treatment.

2. Understand Your Pre-Enactment Balance for Each Employee

Your MPF trustee should provide a statement showing the pre-enactment employer contribution balance for each employee as of 30 April 2025. This figure is critical for calculating future SP/LSP net costs. Keep this documentation as it will be needed when you eventually process any SP or LSP claims.

3. Review Employment Contracts

Some employment agreements may contain clauses that reference the MPF offsetting arrangement or use it in calculations. These references need to be reviewed and updated to avoid confusion or disputes. Any contractual wording that implies the employer will offset SP/LSP using post-May 2025 MPF contributions is now legally void.

4. Check Eligibility for the Government Subsidy

If you employ 200 or fewer people and your annual turnover is within the HKD 400 million threshold, you should register with the Labour Department's subsidy scheme. Do not wait until an SP/LSP claim arises to investigate eligibility. Pre-registration may be required.

5. Update Payroll and HR Systems

Your payroll software or HR system may need to be updated to separately track pre-enactment and post-enactment employer MPF contributions. Many payroll providers have already released updates for this, but it is worth confirming with your provider that the split is being tracked correctly.

Need help with your company's ongoing statutory compliance? Air Corporate provides company secretary and accounting services for Hong Kong businesses of all sizes. Contact our team.

What Has NOT Changed

It is equally important to understand what the abolition did not change:

- The eligibility criteria for severance payment (dismissal after 2 or more years of continuous service) are unchanged

- The eligibility criteria for long service payment (resignation or dismissal after 5 or more years of service, or certain other qualifying events) are unchanged

- The calculation formula for SP and LSP (last monthly salary x 2/3 x years of service, subject to caps) is unchanged

- MPF contribution rates (5% each from employer and employee) are unchanged

- The employee's right to receive their full MPF accrued benefits upon retirement is unchanged

- The employee's MPF contributions remain entirely separate and were never part of the offset mechanism

For the full picture of employee compensation and benefits in Hong Kong, including how MPF interacts with other statutory entitlements, see our comprehensive guide. You may also want to revisit our article on MPF contributions and payment obligations for the underlying mechanics.