Setting up a BVI company remotely is straightforward. The hard part is the bank account. For non-resident founders in 2026, remote account opening depends far more on your business model, documentation quality, and risk profile than on which BVI incorporation provider you choose. This guide covers what is realistically possible, which banking routes work for non-residents, what documents you need, and what to expect from start to finish.

Important note: No provider can legitimately guarantee bank account approval. The bank or EMI always decides independently under its own KYC and AML rules.

Highlights of this article

- A BVI company can be incorporated in 1–3 business days once KYC documents are approved

- Remote bank accounts are possible but not guaranteed: EMIs/digital banks tend to be more accessible than traditional banks for non-residents

- Declines are almost always caused by documentation gaps, not incorrect forms

- Traditional banking takes 3–12 weeks; EMI onboarding typically takes 1–3 weeks

- Air Corporate supports BVI banking through Airwallex, Payoneer, and Aspire (All-Inclusive plan) plus CITIC, HSBC, and OCBC (Expert plan). Note that all plans include banking solutions in Hong Kong or Singapore. Opening a business account in the BVIs is almost impossible

2 routes for remote banking with a BVI company

Non-resident founders have 2 main options for opening an account remotely.

1. Traditional banks

Traditional banks offer broader services: trade facilities, higher limits, and established relationship management. The tradeoff is that they often require in-person meetings, stronger ties to a commercial hub, or clear evidence of operational substance. Compliance review is thorough and can take several weeks to several months.

Best for: BVI companies with documented operations, clear counterparties, and a strong source of funds story.

As of the date of this article, the traditional banks that support bank account opening for a BVI company registered with Air Corporate include: HSBC, OCBC and China Citic banks.

2. EMIs and fintech business accounts

Electronic money institutions (EMIs) are more likely to support fully remote onboarding. They are faster than traditional banks and typically provide multi-currency accounts and international payout tools. Supported countries, currencies, industries, and payout corridors vary by institution.

Best for: founders who need fast remote access to multi-currency payment infrastructure and meet EMI risk requirements.

The partners currently recommended by Air Corporate for the opening of a business account for a BVI company include: Air Wallex, Payoneer and Aspire.

Key KYC terms every BVI founder needs to understand

Banks and EMIs use these terms throughout onboarding. Knowing them before you apply saves time and avoids miscommunication.

| Term | Plain explanation |

|---|---|

| KYC | Know Your Customer: identity and background checks on directors, shareholders, and UBOs |

| AML | Anti-Money Laundering: checks to confirm funds are not linked to financial crime |

| UBO | Ultimate Beneficial Owner: the real person or persons who ultimately own or control the company |

| Source of Funds (SoF) | Where the money moving through the account comes from |

| Source of Wealth (SoW) | How the company owners built their overall personal wealth |

If your SoF or SoW story is vague or not supported by documents, remote banking becomes significantly harder regardless of which incorporation provider you use.

What BVI incorporation providers can (and cannot) do for banking

Most BVI incorporation firms do not open bank accounts for you. What they typically do is:

- Assess whether your profile is likely to qualify for the accounts available to them

- Help prepare the documents and explanations required for application

- Introduce you to banks or EMIs they have working relationships with

- Coordinate submission and follow-ups during the review process

No legitimate provider can guarantee approval. If a provider promises a guaranteed account, treat that as a warning sign.

What Air Corporate's banking support includes

| Plan | Price | Banking support |

|---|---|---|

| Base | USD 1,750 | Not included |

| All-Inclusive | USD 1,850 | EMI introductions: Airwallex, Payoneer, Aspire. Document certification. 1 Certificate of Incumbency. |

| Expert | USD 2,250 | Everything in All-Inclusive, plus traditional bank applications to CITIC, HSBC, OCBC. Priority application handling. 3 hours legal and tax consulting. |

| Annual renewal | USD 955/yr | Ongoing corporate maintenance, economic substance reporting, 24/7 document access |

Ready to open a BVI company with banking support? Compare BVI plans →

Eligibility: who is likely to qualify for remote BVI banking

Banks and EMIs look primarily for clarity and consistency. Before applying, assess where your profile sits.

More likely to be eligible

- Clear business model: it is easy to explain who pays you, why, how you deliver, and how suppliers are paid

- Customers and suppliers mostly in low-to-medium risk countries

- Reasonable and explainable transaction volumes with no sudden unexplained spikes

- Documented operations: contracts, invoices, website, marketplace storefront, or platform dashboard

- Simple and transparent ownership with no unnecessary offshore layers

- Strong SoF and SoW evidence for all UBOs and startup capital

Likely to face additional scrutiny or restrictions

- High-risk sectors: gambling, adult content, unlicensed financial services, certain crypto business models

- Complex structures with multiple layers and no clear commercial rationale for each layer

- Expected activity that resembles pass-through processing with limited operational substance

- Weak documentation: no contracts, no invoices, no credible online presence, no clear counterparties

- Heavy cross-border exposure to high-risk corridors or countries subject to enhanced monitoring

Eligibility is always institution-specific. One EMI may accept a profile that another declines outright.

Why BVI bank account applications get declined

Declines are almost always caused by risk ambiguity, not incorrect forms or missing signatures.

| Decline reason | What it means in practice |

|---|---|

| Insufficient Source of Wealth | Owners cannot show how they built their personal wealth with supporting documents |

| Unclear Source of Funds | No evidence of where incoming account funds will come from |

| Story-document mismatch | You claim "consulting" but contracts show unrelated activity, or invoices do not match expected volumes |

| No proof of operations | No customers, no website, no supplier contracts, no activity track record |

| High-risk geography | Customer or supplier countries trigger the institution's internal risk rules |

| Complex ownership with no rationale | Multiple offshore layers with no clear business reason for the structure |

| Negative screening results | Adverse media matches, sanctions screening flags, or inconsistent identity information |

| Third-party payment flags | "Funds come from partners" language triggers payment facilitation concerns |

How to reduce rejection risk before you apply

- Prepare a one-page transaction flow explanation: who pays you, why, from where, and where the funds go

- Make sure your narrative is consistent across incorporation documents, website copy, invoices, and application answers

- Provide SoF and SoW documentation upfront rather than waiting for the bank to request it

- Apply to the right tool for your situation: use an EMI for international payment infrastructure, a traditional bank when broader services are needed and you are eligible

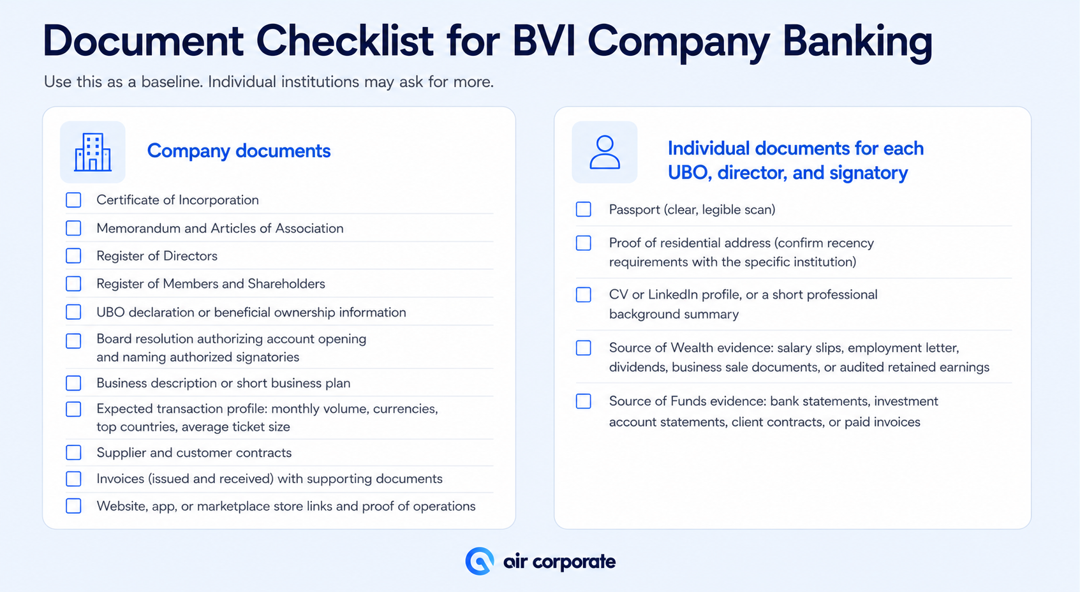

Document checklist for BVI company banking

Use this as a baseline. Individual institutions may ask for more.

Company documents

- Certificate of Incorporation

- Memorandum and Articles of Association

- Register of Directors

- Register of Members and Shareholders

- UBO declaration or beneficial ownership information

- Board resolution authorizing account opening and naming authorized signatories

- Business description or short business plan

- Expected transaction profile: monthly volume, currencies, top countries, average ticket size

- Supplier and customer contracts

- Invoices (issued and received) with supporting documents

- Website, app, or marketplace store links and proof of operations

Individual documents for each UBO, director, and signatory

- Passport (clear, legible scan)

- Proof of residential address (confirm recency requirements with the specific institution)

- CV or LinkedIn profile, or a short professional background summary

- Source of Wealth evidence: salary slips, employment letter, dividends, business sale documents, or audited retained earnings

- Source of Funds evidence: bank statements, investment account statements, client contracts, or paid invoices

If applying to an EMI or fintech account

- Platform statements from Shopify, Amazon, or similar marketplaces

- Fulfilment and logistics provider details

- Refund, returns, and chargeback dispute policy

- Supplier list and main customer categories

Realistic timelines: BVI incorporation and remote account opening

These are planning ranges, not guarantees. Your actual timeline depends on how quickly you supply documents and your risk profile.

| Stage | Best case | Typical | Slow case | Main friction points |

|---|---|---|---|---|

| BVI incorporation | 1–2 days | 1–3 business days | 2+ weeks | KYC clarifications, complex ownership, notarisation required |

| Traditional bank | 3–4 weeks | 6–10 weeks | 12+ weeks | SoF/SoW depth, geography risk, in-person meeting requirement |

| EMI/fintech | 3–5 days | 1–3 weeks | 4+ weeks | Restricted industries, country limits, unclear transaction profile |

What slows banking down most:

- Unclear or inconsistent business model narrative

- Missing contracts, invoices, or website details

- Complex ownership chains without clean documentation

- Higher-risk industries or countries

- Vague or unverified source of funds and source of wealth

Comparing providers: what to look for when choosing a BVI service for remote banking

Not all BVI incorporation providers offer the same level of banking coordination. When comparing options, check for these specific capabilities:

| What to check | Why it matters |

|---|---|

| Do they offer a dedicated banking support service? | An introduction-only provider may leave you doing most of the work |

| Which banks or EMIs do they introduce? | The quality and range of partners determines your options |

| Do they support traditional banks or only EMIs? | Traditional banks provide broader services if your profile qualifies |

| Can they help with SoF/SoW documentation? | This is the most common failure point in applications |

| Do they offer a pre-check before you pay? | A good provider assesses your profile before you commit |

| What does the annual renewal include? | Ongoing support matters beyond the first year |

Air Corporate includes pre-assessment, document preparation, and banking coordination in its All-Inclusive and Expert plans. With 10,000+ companies incorporated, 9,000+ bank accounts opened, and a 95%+ bank account success rate, the team has a strong track record across BVI, Cayman, Seychelles, and Hong Kong structures.

BVI vs Hong Kong for remote banking

Many founders choose BVI for holding or structuring purposes. If your priority is day-to-day operating banking, it is worth comparing BVI and Hong Kong before you commit.

BVI tends to work well when:

- You need a holding structure and your operating activity happens in a separate entity

- You can clearly evidence counterparties and operational flows in the underlying company

- Your banking needs are for international wires and structured holdings, not day-to-day trading

Hong Kong tends to work better when:

- Day-to-day banking and payment operations are the core requirement

- You want a commercial hub that international banks already understand well for trade and services

- Your business has genuine operations and you want the structure to reflect that operationally

- Your suppliers, payment partners, or banking relationships are already in the Asia-Pacific region

Air Corporate supports both BVI company formation and Hong Kong incorporation with end-to-end banking support.