Key Takeaways

- Relevant entities that carry on a relevant activity must meet the economic substance test each year and report through the official portals

- Pure equity holding companies have a reduced test focused on applicable Cayman filings and adequate human resources and premises in Cayman appropriate to holding/managing equity participations.

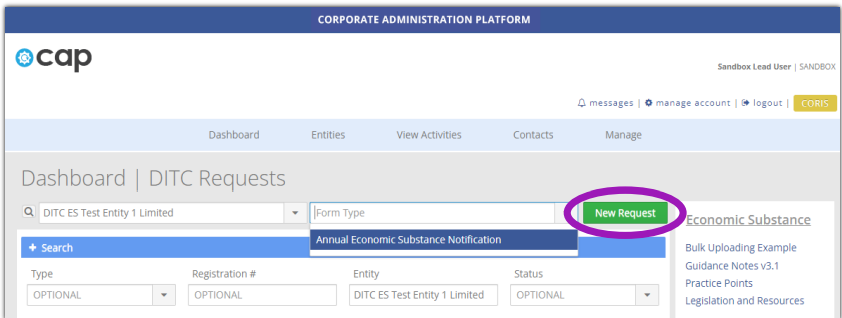

- The Economic Substance Notification (ESN) is filed on the CAP portal and is a prerequisite to the annual return. Due by 31 March each year.

- The Economic Substance Return (ESR) is filed on the DITC Portal within 12 months after financial year end.

- Penalties include KYD 10,000 on a first failure, KYD 100,000 on a second consecutive failure, KYD 5,000 for late ESR plus KYD 500 per day, and criminal offences for false or misleading information.

Overview of Economic Substance Rules in the Cayman Islands

The regime is set out in the International Tax Co-operation (Economic Substance) Act and detailed in Economic Substance Guidance Notes v3.2 (July 2022) and the TIA Enforcement Guidelines (31 March 2022). These define who is in scope, the nine relevant activities, the economic substance test, and how filings are made.

Oversight sits with the Tax Information Authority (TIA), which operates through the Department for International Tax Cooperation (DITC). All filings are made through the CAP and DITC Portal systems.

Who Is in Scope (and Who Is Not)

In Scope: “Relevant Entities”

- Companies under the Companies Act

- Limited Liability Companies (LLCs) under the Limited Liability Companies Act

- Limited Liability Partnerships (LLPs) and partnerships (where applicable)

- Foreign companies registered in the Cayman Islands

Out of Scope or Excluded

- Investment funds (as defined) and entities through which a fund invests or operates

- Domestic companies only doing business in Cayman and meeting the domestic criteria

- Entities that are tax resident outside Cayman and file a Tax Resident Outside the Islands Form (TRO Form) with evidence via the DITC Portal

What Counts as a “Relevant Activity”

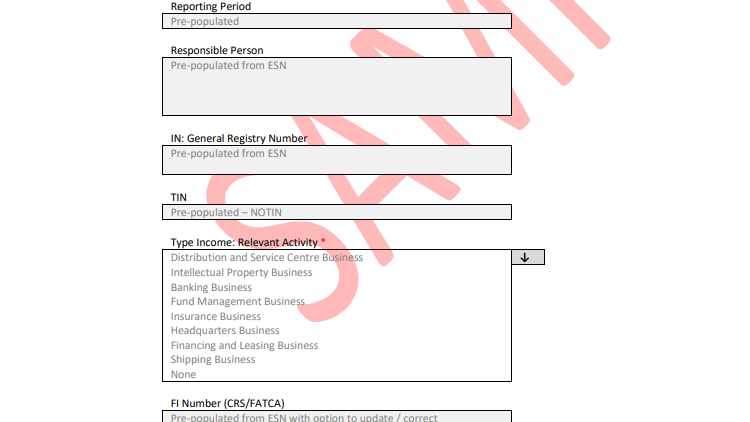

There are nine categories: banking, insurance, fund management, financing and leasing, distribution and service centre, headquarters, shipping, holding company business, and intellectual property business. The Guidance provides Core Income Generating Activity (CIGA) examples for each.

Note

Note

If you conduct more than one relevant activity, assess each activity separately for the test and in your ESR.

The Economic Substance Tests

The Standard Test

You must demonstrate in Cayman:

- Direction and management in Cayman (board knowledge, meetings with quorum in Cayman, minutes and records kept in Cayman).

- Adequacy of expenditure, employees, and premises in Cayman.

- Core Income Generating Activities (CIGAs) performed in Cayman. Outsourcing is allowed in Cayman if you monitor and control the provider.

Reduced Test for Pure Equity Holding Companies

A pure equity holding company satisfies a reduced test by:

- Complying with applicable Companies Act filing and record-keeping requirements, and

- Having adequate human resources and premises in Cayman appropriate to holding and managing equity participations.

Unlike other entities, a pure equity holding company does not need to be directed and managed in Cayman, but it must maintain sufficient local substance for its holding activity.

No Relevant Income in the Year

If a relevant entity conducts a relevant activity but earns no relevant income during the financial year, the economic substance test does not apply for that period.

However, the entity must still:

- File its Economic Substance Notification (ESN), and

- Submit a nil Economic Substance Return (ESR) if a relevant activity was carried on during the year.

Note

Tip

Air Corporate can provide Cayman-based company secretarial support and ensure board minutes and registers are maintained to evidence direction and management.

What to File, Where, and When (2026 Cayman Economic Substance Deadlines)

| Filing | Who Must File | Where to File | Deadline |

|---|---|---|---|

| Economic Substance Notification (ESN) | All entities in scope of the Economic Substance Act (including partnerships noted in the Guidance) | CAP Portal (General Registry) | By 31 March each year – required before submitting the Annual Return |

| Economic Substance Return (ESR) | Relevant entities that carried on a relevant activity during the year | DITC Portal | Within 12 months after the financial year end |

| TRO Form (Tax Resident Outside Cayman) | Entities claiming foreign tax residence | DITC Portal | Within 12 months after the financial year end, with supporting evidence (e.g., certificate of tax residence) |