Profits tax is the main corporate tax in Hong Kong. It applies to assessable profits arising from a trade, profession, or business carried on in Hong Kong. Understanding how it is calculated, what you can deduct, and when it is due is essential for any Hong Kong company.

This guide covers the two-tiered rates, what income is taxable and what is exempt, every deductible expense category, capital allowances, R&D incentives, and the step-by-step calculation of assessable profits. For an overview of how Hong Kong's tax system works, see our corporate tax guide.

Highlights of this article

- Profits tax rates: 8.25% on the first HKD 2 million of assessable profits, 16.5% above. Only 1 company per connected group can use the lower 8.25% rate.

- Only profits arising in or derived from Hong Kong are taxable. Offshore profits are generally exempt.

- Capital gains, dividends from other companies, and interest from licensed bank deposits are not subject to profits tax.

- R&D expenditure qualifies for 100% to 300% deduction depending on type. Capital allowances apply to plant and machinery and industrial/commercial buildings.

- Losses can be carried forward indefinitely but cannot be carried back or transferred between group companies.

- Profits tax is paid after the year ends. Provisional profits tax is collected in advance based on the prior year's liability.

The two-tiered profits tax rates

| Entity type | Profits up to HKD 2 million | Profits above HKD 2 million |

|---|---|---|

| Corporations | 8.25% | 16.5% |

| Unincorporated businesses | 7.5% | 15% |

| Companies with no Hong Kong business (offshore) | 0% | 0% |

The two-tiered regime was introduced for the year of assessment 2018/19. The lower rate (8.25%) is available to 1 nominated entity within a connected group. You cannot split a business across multiple related companies to multiply access to the lower rate.

Companies with only offshore profits pay no profits tax. Whether a company qualifies for offshore status is determined by the IRD based on where profit-generating activities actually take place. See our corporate tax guide for the full offshore exemption rules.

What is taxable and what is not

Taxable income

Profits tax applies to assessable profits from a trade, profession, or business carried on in Hong Kong. This includes:

- Revenue from sales of goods or services where transactions are concluded in Hong Kong

- Royalties received for IP used in Hong Kong

- Management fees for services rendered in Hong Kong

- Commissions from Hong Kong-based activities

Income NOT subject to profits tax

| Income type | Profits tax treatment |

|---|---|

| Capital gains from long-term investments | Exempt |

| Dividends received from other companies | Exempt |

| Interest from deposits with licensed banks in Hong Kong | Exempt |

| Profits from qualifying debt instruments (issued after 1 April 2018) | Exempt |

| Offshore profits (activity outside HK) | Exempt if IRD agrees with the claim |

The capital gains exemption is particularly significant. Profits from selling company shares, property, or other assets held as investments are not subject to profits tax in Hong Kong.

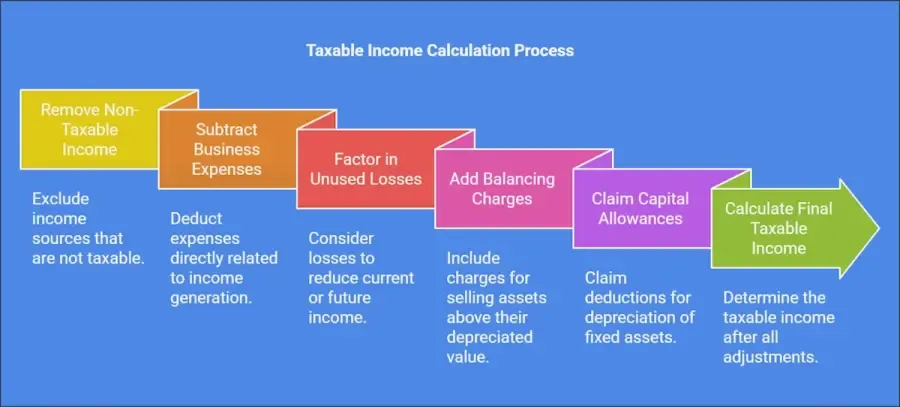

How to calculate assessable profits: 5 steps

Your assessable profits are not simply your accounting profit. The calculation involves a series of adjustments to arrive at the taxable figure.

Step 1: Start with accounting profit, then remove non-taxable income

Begin with your audited profit and loss account. Subtract any income that is not subject to profits tax: capital gains, dividends, exempt interest, and any offshore profits you are claiming an exemption on.

Step 2: Add back non-deductible expenses

Re-add any expenses that were charged in the accounts but are not allowable for profits tax purposes:

- Personal or domestic expenses

- Capital expenditure charged as revenue

- Payments disallowed under Section 17 of the Inland Revenue Ordinance

- Depreciation charged in accounts (replaced by capital allowances in Step 5)

- Expenses not incurred in the production of chargeable profits

Step 3: Deduct allowable business expenses

Subtract all expenses that were incurred in producing the chargeable profits. Allowable deductions include:

| Deductible | Not deductible |

|---|---|

| Salaries, wages, bonuses, MPF contributions | Personal or domestic expenses |

| Office rent, rates, and utilities | Capital improvements |

| Professional fees (legal, accounting, audit) | Fines and penalties |

| Business travel and client entertainment | Income tax paid in other jurisdictions |

| Repairs and maintenance of business assets | Commuting costs (home to workplace) |

| Charitable donations (up to 35% of adjusted profits) | Expenses under Section 17 IRO |

| Interest on borrowings for business purposes | Provisions not yet incurred |

| Costs of IP acquisition (patents, trademarks, copyrights) | Spouse or partner benefit payments |

| Foreign taxes paid on the same income | Reserves or contingency funds |

Step 4: Apply loss offsets

Deduct any unrelieved losses carried forward from previous years of assessment.

Loss carryforward mechanics:

- Losses can be carried forward indefinitely. There is no time limit on how many years a loss can be held.

- Losses cannot be carried back to offset profits in previous years. The IRD does not allow retrospective loss relief.

- Losses cannot be transferred between group companies. Each company's losses are ring-fenced. A profitable sister company cannot absorb another company's losses.

- Losses are offset against the first available profits in subsequent years. You cannot choose to skip a year of offsetting to preserve losses.

- If a company changes its principal business activity, the IRD may challenge whether pre-change losses are still available for offset. Maintain records showing continuity of business purpose.

Nil return vs loss return, key distinction:

| Return type | When to file | What it means | What to check |

|---|---|---|---|

| Nil return | Zero assessable profits (no profit and no loss, or losses exactly offset profits) | Company had activity but made no net taxable profit | Confirm all disallowances and allowances are correctly applied |

| Loss return | Assessable profits calculation results in a net loss | Company can carry the loss forward to offset future profits | Loss is preserved in IRD records; no tax due |

| Zero activity return | Company was dormant or had no business activity | Still mandatory to file; explain the zero activity | Keep SCR and statutory records up to date |

Both nil returns and loss returns are mandatory. A company that had zero revenue must still file BIR51 and is not exempt simply because there is no tax to pay. Failure to file is an offence regardless of the financial result.

Step 5: Claim capital allowances

Replace accounting depreciation with IRD capital allowances. Capital allowances are prescribed deductions for the wear and tear of qualifying assets. Hong Kong uses a pooling system with three depreciation classes:

Class 1 pool (30% annual allowance)

Assets: Computers and peripheral equipment, software, data communication equipment, photocopiers, cash registers, fax machines.

Class 2 pool (20% annual allowance)

Assets: Motor vehicles, most plant and machinery not in Class 1 or Class 3, production equipment, refrigeration equipment, lifts and escalators.

Class 3 pool (10% annual allowance)

Assets: Office furniture, partitions, lighting, air conditioning systems, built-in equipment, fixtures and fittings.

| Asset class | Examples | Initial allowance (year 1) | Annual allowance (reducing balance) |

|---|---|---|---|

| Class 1 | Computers, software, servers | 60% | 30% |

| Class 2 | Vehicles, plant, machinery | 60% | 20% |

| Class 3 | Office furniture, fittings, fixtures | 60% | 10% |

| Industrial buildings | Factories, warehouses | 20% | 4% |

| Commercial buildings | Offices, retail units | None | 4% |

How pooling works: Within each class, all qualifying assets are pooled together. The total written-down value of the pool is carried forward year to year. New assets added to the pool in a year receive the initial allowance (60%) on their cost; the remaining balance goes into the pool for annual allowances at the class rate.

Worked example, Class 1 pool:

- Year 1: Buy HKD 100,000 of computers

- Initial allowance (60%): HKD 60,000 deducted in year 1

- Remaining pool value: HKD 40,000

- Annual allowance (30%): HKD 12,000 deducted in year 2

- Pool carried forward: HKD 28,000

Total deduction over 2 years: HKD 72,000 out of HKD 100,000 cost.

Balancing charge on asset disposal

When an asset is sold, the sale proceeds are deducted from the pool. If the disposal proceeds exceed the pool's written-down value, a balancing charge arises: the excess is added back to assessable profits in the year of disposal.

Worked example:

- Pool written-down value at start of year: HKD 28,000

- Asset sold for HKD 45,000

- Balancing charge: HKD 45,000 - HKD 28,000 = HKD 17,000 added to assessable profits

Conversely, if the entire pool is disposed of for less than the written-down value, a balancing allowance is granted for the shortfall (a final deduction).

Once all 5 adjustments are made, the result is your assessable profits. Apply the appropriate rate (8.25% or 16.5% for corporations) to arrive at your profits tax liability.

R&D tax deductions

Hong Kong offers enhanced deductions for qualifying research and development expenditure:

| R&D type | Deduction rate | Conditions |

|---|---|---|

| Type A | 100% | General R&D expenses directly related to the business |

| Type B | 300% on first HKD 2 million, then 200% | Qualifying local R&D performed in Hong Kong |

Eligible R&D costs include salaries for dedicated R&D staff, consumables used in research, payments to designated local research institutions, and capital costs (excluding land and buildings).

To qualify for Type B, the R&D activity must be carried out in Hong Kong and aim to improve or develop new products, services, or processes with genuine scientific or technical value.

Industry-specific tax incentives

Qualifying debt instruments

- Issued before 1 April 2018: subject to 50% of the standard profits tax rate

- Issued on or after 1 April 2018: fully exempt from profits tax

Aircraft and ship leasing

- Ship leasing companies: exempt from profits tax

- Ship leasing managers: taxed at 8.25%

- Aircraft leasing and management: taxed at 8.25%

Corporate Treasury Centres (CTCs)

Companies qualifying as a Corporate Treasury Centre can apply a concessionary rate of 8.25% on profits from qualifying treasury activities. This is a separate regime from the two-tiered system and requires IRD approval.

Filing obligations and deadlines

The IRD issues Form BIR51 (Profits Tax Return) on 1 April each year. The deadline depends on your financial year end:

| Financial year end | Filing deadline | Extension available |

|---|---|---|

| April to November | 2 May (1 month after issue) | No. Apply in writing if needed. |

| December | 15 May (extended) | Via tax representative bulk extension |

| March | 15 November (extended) | Via tax representative bulk extension |

For a newly incorporated company, the first BIR51 is typically issued approximately 18 months after incorporation. From the second year onwards, returns are issued each April.

The return must be accompanied by audited financial statements, a tax computation, and supplementary forms. For the full step-by-step filing process, see our profits tax return guide. For the difference between the Profits Tax Return and the Annual Return, see our Annual Return vs Profits Tax Return guide.

Audit exemption for small companies

If your company's gross revenue does not exceed HKD 2 million for a financial year, you are not required to file audited accounts with the IRD for that year. However, the IRD can request audited accounts at any time, and dormant companies that have formally declared dormancy to the Companies Registry are separately exempt.

Provisional profits tax

Because the exact profits tax liability is only known after the financial year ends, the IRD collects an advance payment called provisional profits tax. This is typically based on 100% of the prior year's final tax liability, billed in 2 installments:

- First installment: 75% of the provisional amount (typically January to March)

- Second installment: 25% (typically 3 months later)

If your current year profits are expected to be at least 10% lower than last year, you can apply to hold over part or all of the provisional tax. For the full application process and deadlines, see our provisional tax holdover guide.

Penalties for non-compliance

Failure to file BIR51 or filing an incorrect return can result in:

- Progressive financial penalties

- The IRD estimating your profits and assessing tax on that estimate (often higher than the actual amount)

- Criminal prosecution in serious cases

The IRD treats tax return filing as a hard statutory obligation. Apply in writing for any extension before the deadline, not after.

Your company secretary does not prepare the profits tax computation or file BIR51. Tax filing is handled by your accountant or tax representative.

Air Corporate handles audit and tax filing for Hong Kong companies from USD 580/year. This includes CPA-audited financials, profits tax computation, BIR51 submission, and provisional tax management.Get started